Construction Robotics Report 2026

(By Zacua Ventures, along with Hilti Ventures and 94 Ventures)

Three years ago we published a detailed look at construction robotics. At the time, it was mostly a story about pilots, prototypes and promise.

Since then, three things have changed:

- Robotics and AI moved up a level. Robots are no longer limited to carefully scripted motions in safe corners of factories. Modern perception, planning and learning systems are more forgiving of dust, clutter and half-finished spaces.

- Construction’s constraints tightened. Labour is older and harder to replace, safety expectations are higher, and the energy transition plus infrastructure programmes are pushing more complex work through the system.

- A first wave of construction robots proved they can survive on real jobs. Layout printers, excavator autonomy kits, rebar robots and digital capture platforms have gone from one-off demos to ‘things we bring back on the right projects’.

Robots are still a tiny line item in global construction spend. Estimates for on-site construction robotics revenue sit in the low single digit billions of dollars globally, growing at roughly mid-teens annual rates. That is not a bubble. It is steady compounding from a very small base.

The point of this report is simple:

Capture where construction robotics actually stands in 2026, in a way that a GC, a trade contractor, an OEM or a founder can pick up, read in one sitting, and refer back to as they build.

We focus on:

● What changed in robotics in general and why that matters on a jobsite

● How the construction robotics market really breaks down

● Four workflows where robots are genuinely working today

● What is inside these machines and where the real technical edge comes from

● Patterns from deployments that worked and those that did not

● A practical cheat sheet for people actually building projects

Executive summary

Robots are no longer a handful of pilots on innovation decks. They are repeat tools in layout, solar piling, rebar tying and reality capture – still a tiny slice of global spend, but with real utilisation and ROI.

- Construction robotics is in repeatable production.

Case studies across layout, rebar tying, solar groundworks and autonomous scanning now show material labour savings (often 30–50% and higher in some deployments), 15–25% faster cycles on the affected scopes, and meaningful rework reductions - The winners focus on bounded, high-utilisation tasks.

The robots that stick do a narrow job extremely well, run often, and plug into existing workflows instead of trying to automate the whole site. - Safety and data, not novelty, drive adoption.

Removing dust, overhead work and repetitive strain sells faster than pure cost claims. At the same time, robots generate structured, BIM-linked data that feeds QA/QC, forecasting and insurance – data is becoming the real moat. - Human-robot teaming is the default operating model.

Field staff are already shifting into – robot technologist roles: planning missions, supervising fleets and interpreting telemetry rather than doing every task by hand. - RaaS and outcome-based pricing fit construction better than CapEx.

Subscription and – per m² / per pile / per scan contracts align with project budgets and risk, and are emerging as the dominant model for serious deployments. - Capital and policy are tilting toward embodied productivity.

Investors are paying up for heavy-equipment autonomy, renewable and civil workflows, and reality capture, while treating installation and MEP robots as earlier-stage bets with high upside. Safety and robotics guidance from regulators and insurers is starting to formalise how these systems show up on jobs. - The next decade hinges on manipulation, not movement.

Locomotion and perception are good enough for many sites; the hard frontier is building with precision: fastening, finishing and assembling in messy, real-world conditions. - Humanoids are hype; task robots are real. Humanoids will likely see targeted use in controlled environments and certain factory or logistics roles. On rough, dynamic construction jobsites, specialised machines will remain the workhorses.

- What this report gives you.

A workflow-by-workflow map, market sizing and outlook, a view into what is actually inside these machines, and a practical playbook for GCs, trades, OEMs and founders who want to move from one-off pilots to portfolio-level advantage.

Construction Robotics Market Map (2026)

2. The robotics moment, and why construction cares

You do not need to love robots to feel the shift. It shows up in news about humanoids, factory automation, warehouse robots, and embodied AI. Under all that noise, there is a simple story.

2.1 Four waves of robotics in one picture

If you zoom out over the last forty years, robotics has gone through four broad waves:

- Industrial arms in cages

- Fixed robots, scripted motion, no people nearby

- Automotive and electronics factories

- Amazing repeatability, zero tolerance for surprise

- Mobile robots and cobots

- Warehouse robots that move shelves

- Robots that safely work next to people on lines

- Better sensors and mapping, still in fairly clean environments

- Data-driven robots

- Cameras and deep learning for perception

- Policies learned from data instead of hand-written rules

- Robots that can tolerate more mess and variation

- Embodied AI and robot foundation models

- Large models trained across many robots and many tasks

- Language and vision used to guide action

- The same “brain” can be adapted to different robot bodies

Construction mostly lives between wave 2 and wave 3 today, with early influence from wave 4. That is enough to change what is realistic. Over the next decade, the technical frontier in construction will be manipulation rather than locomotion: precise drilling, fastening, placing and finishing in messy, semi-structured environments, not just moving safely through space.

You no longer need an army of PhDs and five years of custom code to get a robot to follow a line on a slab, track a trench, or find rebar intersections under dust and shadow. You can stand on top of what the broader robotics ecosystem has already built.

2.2 Hardware, compute and capital caught up

A few other trends make this moment different from the last hype cycle:

- Embedded compute is now powerful enough to run good perception and planning models on mobile platforms and heavy machinery. What used to require a server rack can now sit on a layout robot or inside an excavator box.

- Sensors and actuators are cheaper and more reliable thanks to the automotive, drone and warehouse industries. Lidar, depth cameras, IMUs and efficient actuators that were once exotic are now off-the-shelf for robotics teams.

- Capital for embodied AI has created a broader ecosystem of tools, standards and expectations around robots working near people. Even if a construction robot is not a humanoid, it benefits from better simulation tools, safety thinking and components.

Construction does not get a free ride from this, but it no longer operates as an island. It can borrow. Capital is already voting this way: investors are paying up for autonomy in proven layout, piling and scanning workflows, while treating interior, MEP and façade robots as earlier-stage, higher-risk bets.

3. The construction robotics market

Before diving into workflows, it is worth grounding the numbers.

3.1 How big is this, really?

Analysts disagree on exact figures because they draw the boundary around construction robot differently. Some include only on-site robots. Some blend in factory automation for building products. Some include drones, some do not.

If you strip that noise away:

- On-site construction robotics is a small but real global market in the low single digit billions of dollars

- It is growing at roughly mid-teens annual rates

- It is still a rounding error on global construction spend, but it concentrates in a handful of workflows where it matters a lot

Bottom-up market sizing by workflow

Revenue by workflow

Construction robotics in 2025 represents less than 0.03 percent of global construction spend. That is not a failed market. It is a market at the beginning of an adoption S-curve. Our estimates are most sensitive to penetration rate assumptions, which rest on private vendor data. If vendors overstate deployment breadth, our figures are high. If Gulf and data centre acceleration exceeds our base case, 2030 estimates are conservative by 30 to 40 percent.

Venture Funding YOY in Construction Robotics (Pitchbook Data)

Construction robotics pulled in $1.36B of venture funding in the first three quarters of 2025, up 125% from the $612M raised in all of 2024 and equal to 37% of all construction-tech capital in that period. Those numbers look like a boom, but the distribution matters. Field AI’s $314M Series B accounts for about 23% of the total. The remaining 22 companies shared roughly $1.05B, or ~$48M per company, solid Series A/B territory, but not a uniform late-stage breakout across the category.

The split by workflow tells the real story. Heavy-equipment autonomy and reality capture raised about $98M and $112M per deal on average in 2025, while installation and task-execution robots averaged ~$27M across six rounds. Investors are pricing earthmoving and surveying autonomy as high-conviction, later-stage bets, and installation / MEP automation as earlier-stage risk where evidence is still building. That 3.5-4× gap in average round size should narrow as interior, MEP and installation robots accumulate the deployment history that layout and civil autonomy already have.

The 37% share of overall ConTech funding is also a reallocation signal. Capital has shifted away from the broad software themes that dominated 2022-2023 – project management, estimating, compliance, and toward machines that change work on site. Whether that persists into 2026 depends on one thing: do installation, finishes and MEP robots start to show the same repeat-purchase and portfolio-rollout patterns that layout printers, solar trenchers and piling systems now exhibit?

3.2 Eight primary workflow families

Most reports slice the market into functions like material handling or demolition. That is useful for analysts but not for people running jobs.

On site, work clusters into eight workflow families that show up again and again:

- Layout and measurement

Robots that translate BIM and coordination models into full-scale marks on slabs and decks. - Groundworks and earthmoving

Autonomy kits and machines that trench, grade, compact or drive piles, especially on solar and linear projects. - Structural and concrete

Rebar robots and other systems that support reinforcement and deck work. - MEP and utilities

Robots that drill, cut, fasten and route cable, conduit and ductwork. - Envelope and facade

Systems that help install façade brackets, panels and glazing, or work safely at height for cleaning or sealing. - Interiors and finishes

Drywall finishing, sanding, painting and flooring assistance, mainly in repetitive interior spaces. - Inspection and digital capture

Drones, rovers and crawlers that follow repeatable routes to collect consistent visual or scan data. - Energy and linear infrastructure

Specialised robots for solar arrays, transmission lines, tunnels and pipelines.

Today, the bulk of actual revenue is in:

- Layout and measurement

- Groundworks and earthmoving

- Structural / rebar

- Inspection and digital capture

The bulk of startup activity is in:

- Interiors and finishes

- MEP and utilities

- Envelope and façade work at height

(Visual will show:)

- Revenue today and likely revenue in 2030 by workflow family

- A “startup density” signal for each

- Logos of representative companies in each cluster

3.3 Regional differences in adoption

Construction is local. Robotics adoption reflects that:

- Asia-Pacific

- Japan and parts of East Asia face acute labour shortages and ageing workforces

- Governments actively support automation in construction (for example, China’s Made in China 2025 and follow-on intelligent manufacturing initiatives)

- Robots are pulled into projects by demographic pressure and policy

- Europe

- Strong regulation on safety, energy and emissions

- Push for industrialised construction and prefabrication

- Robotics is often wrapped into digital construction and off-site strategies

- North America

- Deep startup ecosystem and strong interest from large GCs and trades

- Highly fragmented codes and labour rules

- Adoption is uneven and often concentrated in a subset of contractors who are comfortable being early but not reckless

For vendors and investors, this matters: the same robot can be sold as a compliance enabler in one region, a labour solution in another, and a productivity and safety tool in a third.

4. From project to robot: how to think about ‘robotable’ work

You cannot evaluate robots in the abstract. They only make sense in the context of actual work on actual projects.

4.1 Seven phases that repeat across projects

Every project has its quirks, but most work falls into these phases:

- Preconstruction and site prep

- Groundworks and foundations

- Structure

- Envelope

- MEP rough-in

- Interiors and finishes

- Commissioning and handover

Robots do not care about contracts or package names. They care about what the work actually looks like on the ground: where things are, how they move, how often they repeat, and how much chaos is around them.

4.2 What makes a task robotable

From live deployments and failures, three properties show up again and again in tasks that are good candidates for robotics:

- Repetitive structure

- The task follows patterns that can be described in simple geometric or rule-based terms

- Examples: printing layout lines from a model, trenching at constant depth and offset, tying rebar at grid intersections

- Physical strain or safety exposure

- The job is bad for bodies or genuinely dangerous, even if crews are careful

- Examples: overhead drilling, heavy repetitive lifting, working at slab edges in wind

- Direct impact on schedule or quality

- If this goes wrong or late, many other things go wrong or late

- Examples: incorrect layout, slow rebar holding pours, missing documentation at handover

Where these three overlap, robots tend to find a home first. The tasks that score highest on all three tend to become the next decade’s task families for robotics: layout, piling, finishing and scanning, each deep enough to support specialised machines and service businesses rather than general-purpose robots.

4.3 Three simple archetypes

Most current construction robots fall cleanly into one of three archetypes:

- Plotters

Turn digital plans into physical reality at full scale- Layout printers on slabs

- Robots that drill or place elements directly from models

- Grinders

Take over brutal, repetitive work- Rebar tying gantries

- Autonomous trenching on solar farms

- Interior sanding and surface preparation

- Scouts

Move around to collect data, not to manipulate the environment- Drones flying repeatable paths

- Mobile scanners inside buildings

- Crawlers in pipes or confined spaces

Thinking in these terms helps cut through marketing language. Every robot claiming to be a ‘platform for autonomous construction’ is usually, in practice, a plotter, grinder or scout aimed at a specific niche. Across all three archetypes, the most durable robots are designed for high utilisation on a narrow slice of work, not generality; they succeed when they can run often, generate consistent data, and slot cleanly into existing crews and schedules.

5. Four workflows where robots are real today

This section looks at four workflows where robots are not only possible but have repeat deployments with real contractors:

- Layout and measurement

- Groundworks and earthmoving

- Structural and rebar

- Inspection and digital capture

Workflow robotability assessment

5.1 Layout and measurement

On-site reality

Layout crews pull points and lines from models or drawings and mark them on slabs and decks. They do this under time pressure, often while working around other trades and equipment. Mistakes propagate into framing, MEP, and finishes.

What robots do

Robotic layout systems:

- Take coordinated layout data directly from BIM or CAD

- Use survey control to align themselves with the project coordinate system

- Move across slabs and decks printing or marking walls, penetrations and hangers at full scale

The most visible example is Dusty Robotics’ FieldPrinter, which has been used by large GCs on commercial projects in North America. A typical pattern:

- VDC exports a layout set

- The FieldPrinter registers to control points

- It prints multi-trade layouts in one pass

- Downstream crews frame and install off the printed markings

Other systems blend advanced total stations, mobile bases and software, but the underlying idea is the same.

Why this works

- The geometry is already digital

- The task is repetitive but structured

- The cost of errors is obvious to everyone

Layout crews spend 3 to 5 percent of project labour hours marking models into physical reality. Human accuracy under site conditions runs to plus or minus one-quarter to one-half inch. Robotic systems connect directly to coordinated BIM exports, register to survey control points, and print multi-trade layouts in a single pass. Three preconditions are non-negotiable: a frozen, coordinated model with a named digital owner; accurate and undisturbed survey control; and a VDC lead with authority to enforce both. When these fail, the robot prints the wrong thing accurately, which is worse than not printing at all.

Unit economics: a two-person survey crew costs $1,400 to $2,200 per day. The Dusty FieldPrinter covers 40,000 to 70,000 square feet per shift versus 8,000 to 15,000 for a human crew, at documented accuracy below plus or minus one-eighth inch. On a 500,000 square foot project, schedule compression of 7 to 10 days translates to $25,000 to $50,000 in direct savings against a subscription cost of $8,000 to $12,000 per month. Economics close firmly above 150,000 applicable square feet per month.

Case Study – DPR Construction – scaling robotic layout on complex projects

DPR Construction, a self-performing general contractor focused on complex and technical projects in healthcare, life sciences, advanced technology, commercial and higher education, has been one of the earliest backers and adopters of robotic layout. Through its venture arm WND Ventures, DPR invested in Dusty Robotics and deployed the FieldPrinter on hospital projects to print multi-trade layouts directly from BIM on the slab. Public case material highlights two effects: layout cycles that compress from days to hours and multi-trade coordination that improves because every crew works off the same full-scale digital print, not overlapping chalk from different teams. For DPR, robots fit into an existing self-perform model rather than replacing it: layout crews shift from pulling points to supervising and sequencing the printer across larger areas of the job.

Source:https://www.dpr.com/media/blog/dpr-and-dusty-robotics-collaborate-to-set-up-success-for-craft

Raise Robotics takes a different approach to the same problem: a multipurpose platform that handles layout, drilling, and facade bracket installation from a single mobile base, purpose-built for slab edge and high-risk environments where a dedicated layout robot cannot safely operate. The St. Jude Children’s Research Hospital deployment, 10,000-plus glass panel positions laid robotically, validated the multi-tool model at production scale.

Source – https://raiserobotics.ai/portfolio/st-jude-childrens-hospital/

5.2 Groundworks and earthmoving

On-site reality

Groundworks on large energy and infrastructure projects involve long runs of trenching, grading, compaction and piling. The work is machine-heavy, repetitive and subject to safety risks, particularly around trench stability and interactions with other equipment.

What robots do

Autonomy kits for heavy equipment:

- Retrofit standard excavators, dozers or dedicated piling rigs

- Use sensors and software to follow predefined paths and depth profiles

- Log work as they go for QA and documentation

On solar farms, for example, autonomous pile drivers can install foundations along hundreds of rows with consistent spacing and depth, often operating longer shifts than human operators could sustain.

Why this works

- Sites are often fenced and controlled

- Geometries are highly repetitive

- The economics of better utilisation on expensive machines are clear

Many of these systems are sold not as robots but as advanced control systems or autonomy kits. That framing matters when you are trying to win over fleet managers and field superintendents.

Solar is the primary driver. Global installations exceeded 380 GW in 2025. A 100 MW facility requires 50,000 to 80,000 piles across a regular grid, with addressable pile installation labour of $400,000 to $960,000. Autonomous kits retrofit excavators and pile rigs to follow predefined paths and depth profiles. Results on qualifying solar sites: installation rates 25 to 40 percent above manual, pile positioning variance below plus or minus one-half inch versus plus or minus 2 to 3 inches manually, and rework rates below 0.5 percent against the 3 to 4 percent manual baseline. These economics do not generalise to urban civil work or sites with complex underground utilities. The market is solar-heavy today and through at least 2028.

Gravis Robotics develops retrofit autonomy for earthmoving equipment, focusing on supervised autonomy modes that let operators switch between manual control and assisted execution. The thesis fits the scaling path we see across civil: upgrading the installed base often expands faster than introducing entirely new machine categories, especially when contractors can standardize deployment across fleets and sites. Public trials, including an autonomous excavator trial with a major contractor at Manchester Airport, show how this category matures through structured field programs rather than one-off demos.

Source – https://www.gravisrobotics.com/

5.3 Structural and rebar

On-site reality

Rebar installation is heavy, repetitive and time-sensitive. Crews are exposed to awkward postures, trip hazards and weather, and the work sits close to the critical path of pours.

What robots do

Rebar robots:

- Span a portion of a deck or mat with a bridge-like frame

- Use cameras and sensors to detect intersections

- Move a tying head across the grid, securing ties according to a set pattern

- In some systems, cooperate with robots that lift and place bundles

The combination of rebar placement and tying delivers:

- Fewer person-hours spent bent over grids

- More predictable output per shift

- Cleaner documentation of what was tied, where and when

Why this works

- Patterns are regular

- Strain and injury risk are high

- The relationship between rebar progress and pours is very visible to everyone on site

Here, robots are adopted most readily by specialist reinforcement and concrete contractors who own that scope across many projects and can build repeatable deployment playbooks.

Reinforcing ironworkers carry some of the highest occupational injury rates in construction. On a 200,000 square foot industrial mat, a crew of 12 to 15 spends 8 to 12 days on tying, directly on the pour critical path. TyBot ties 300 to 450 intersections per hour against a skilled ironworker’s 40 to 80. On a 200,000-intersection mat, this compresses a 12-day sequence to 4 to 6 days. At $90 to $120 per hour fully loaded and a crew of 12, the labour saving is $65,000 to $115,000. Deployment cost runs $35,000 to $55,000. Net saving is $10,000 to $80,000 plus critical path recovery. Robots require pre-deployment geometry review to distinguish regular zones from complex zones; skipping this step is the most common cause of schedule model failures on rebar deployments.

5.4 Inspection and digital capture

On-site reality

Jobs already rely on photos, drone shots and scans, but the coverage is inconsistent. It depends on who was on site that day and what they chose to document.

What robots do

Digital capture robots:

- Fly repeatable routes as drones over roofs, facades, earthworks and large sites

- Drive repeatable paths through corridors and rooms with 360 cameras or lidar

- Traverse pipes or hard-to-reach spaces with crawlers

They produce regular, structured data that feeds:

- Progress dashboards

- QA and clash detection

- Claims support

- As-built documentation and digital twins

Because these systems only sense, not manipulate, they often reach maturity faster than fully task-executing robots.

A structured robotic capture programme combining weekly drone flights with monthly interior scanning on a $50 million project costs $3,500 to $5,500 per month. Conservative claim avoidance value from documented construction litigation data runs at $80,000 to $150,000 per project in expected value. Payback in most cases is under six months. The structural risk is platform absorption within three to five years as Procore, Autodesk, and Trimble integrate capture as standard project management infrastructure.

N Robotics, a Zacua portfolio company, sits between quadruped platforms and drone-only capture by offering mobile robots with configurable sensor payloads. The product logic matches the way capture demand fragments across phases: the same base robot can support progress documentation, environmental monitoring, and constrained inspection by swapping payloads rather than mobilizing entirely different systems.

Source – https://www.nrobotics.com/

Track3D complements this stack on the software side: a reality intelligence platform that turns routine capture into schedule- and BIM-relevant signals, with modules designed around progress tracking and deviation detection workflows. This pairing matters because capture value compounds only when it becomes repeatable, structured, and integrated into the project’s operating cadence.

Source – https://track3d.ai/

Case Study – Hensel Phelps and Trimble – Reality Capture with Spot

Hensel Phelps, an employee-owned general contractor that plans, builds and manages facilities across aviation, technology, federal and other sectors, has been out in front on robotic reality capture. The firm worked with Trimble and Boston Dynamics to deploy Spot equipped with a laser scanner on live projects, using autonomous missions to collect repeatable point clouds for QA and progress tracking. In published feedback, Hensel Phelps’ VDC team highlights reduced rework risk and more consistent documentation, describing the robot-scanner combo as a practical way to keep models and field conditions aligned.

Source: https://www.therobotreport.com/spotwalk-gathers-construction-data-holobuilder-boston-dynamics/

5.5 Other emerging workflows

The workflow table earlier includes several rows that are not yet in the main text: rebar with complex geometry, MEP in repetitive buildings, and interiors and finishes. All three are moving, but at different speeds.

Rebar in complex geometry

Beyond large, regular mats, the next step is reinforcement in congested, irregular zones and eventually vertical elements. These areas combine high safety exposure with messy geometry, which makes them harder to robotise cleanly.

Spacer Robotics’ GRID system is an example of where this is going: an autonomous rebar-tying robot built around sensor fusion, SLAM and lidar, designed for long-duration, high-throughput tying rather than one-off spot tools. As systems like this prove themselves beyond textbook mats, they will test how far autonomy can stretch into the more awkward reinforcement patterns that dominate real projects.

Source – https://www.spacerrobotics.ai/

MEP in repetitive buildings

In hotels, student housing, data centers and logistics facilities, MEP rough-in follows patterns tight enough for robots to help. Systems like Hilti’s Jaibot and early-stage platforms from CSC Robotics and others take BIM-coordinated hanger and sleeve points and turn them into precise overhead drilling and marking. The robotable zone is the repetitive field of rooms or racks; risers, plant rooms and late-stage coordination clashes still sit with human crews. Where projects repeat the same room types hundreds of times, early data suggests overhead drilling automation can shift weeks of ceiling work into days for a trained team.

Case Study – Hilti – Overhead Drilling with Jaibot

Hilti is a global leader in providing innovative tools, technologies, software and services for the construction industry, and its Jaibot robot is a clear example of that push. Jaibot is a semi-autonomous ceiling-drilling robot that takes BIM data, locates itself indoors via a positioning system and executes overhead drilling for mechanical, electrical and plumbing layouts in a dust-controlled way. On projects such as NREL’s research facility in Colorado, Jaibot has been used alongside human crews to take over the most strenuous overhead work, addressing labor shortages while improving ergonomics and consistency for MEP installations.

Source – https://www.hilti.com/content/hilti/W1/US/en/business/business/trends/jaibot.html

Hardhat Robotics is targeting this space by automating repetitive electrical tasks in data-heavy environments like data centres, treating electrical installation as a workflow that can be partially automated and instrumented rather than a purely manual trade.

Source – https://hardhat-robotics.com/

Interiors and finishes

Drywall finishing, sanding and painting remain ergonomically brutal and highly repetitive, especially in long corridor projects and standardised units. Canvas, Finish Robotics and similar systems target the ‘big, boring rectangles’: long runs of board and large open walls. Robots spray, sand or trowel to a consistent specification, while humans handle corners, penetrations and small corrections. The payback story is a mix of steadier throughput, reduced punch lists and lower wear on tapers and painters. This category sits in pilot-to-early production today, but it scores well on geometric regularity and low safety exposure, which is why many contractors treat it as their next experiment after layout or scanning.

Origin is one of the teams leaning into this with a general-purpose interior robot and a modern AI-stacked autonomy layer rather than a single-task gadget. The bet is that the same mobile platform can handle drywall finishing and related workflows across similar units and floors, with perception and planning systems doing more of the heavy lifting over time.

Source: https://origin.tech/

6. What is actually inside these machines

At first glance, construction robots can look wildly different. Under the hood, their structure is surprisingly similar.

You can think of five layers:

- Sensing

- Cameras for recognising edges, lines, bars, equipment, people

- Range sensors like lidar for mapping obstacles and open space

- IMUs and encoders to keep track of motion

- Localisation

- Survey control and total stations to anchor to project coordinates

- SLAM for building a local map while moving

- GNSS / RTK on large outdoor sites with clear sky

- Planning and control

- High-level decisions about what to work on next

- Low-level control loops that move actuators precisely and safely

- Human interaction

- Interfaces that crews can actually use under time pressure

- Clear states: idle, active, paused, fault

- Simple, safe ways to pause or stop work when needed

- Data and learning

- Logs of sensor data, operations, faults and context

- Analytics that track utilisation, downtime, production

- Feedback loops that improve models and behaviours over time

Over time, this data exhaust becomes the real moat: better datasets drive better models, which drive higher autonomy and utilisation, which in turn create more data. Hardware can be copied; long-running, task-specific data loops are harder to match.

The interesting shift in recent years is where differentiation lives.

- Ten years ago, every serious team had to build most of this stack themselves

- Today, many components are standardised or borrowed from other industries

- Real edge increasingly comes from:

- Deep understanding of a specific workflow

- Robustness in real conditions, not in a demo

- Integration into existing tools and processes

- The ability to learn and improve across projects

For decision-makers in construction, this means good questions are less about – what AI model do you use? and more about – how does this fit into what we already do, and how do we get better together over time.

7. What we have actually learned from deployments

We now have enough live projects across layout, rebar, earthmoving and digital capture to move beyond theory. A few patterns show up consistently.

7.1 What successful deployments have in common

- The robot has a sharp, narrow job.

Everyone on the project can answer, in one sentence, what the machine does and what it does not do. - Someone on the contractor side owns it.

This is often a superintendent, a VDC lead or a trade manager. They:

- Schedule it

- Make sure the site is ready

- Handle small issues

- Act as the bridge between crews and vendor

- It is planned like a piece of key equipment, not a guest.

Robotic tasks sit on the schedule. Logistics plans account for space, power and access. Digital inputs have clear owners.

In the background, a new role is emerging on successful projects: field technicians who understand both the work and the machines, effectively acting as ‘robot technologists’ who keep fleets productive rather than swinging tools full-time.

- Feedback is treated as input, not complaint.

Crews are encouraged to be blunt. Vendors and contractors review deployments and adjust playbooks. Data is used, not just stored.

7.2 Why some pilots never turn into real adoption

Common failure modes:

- Innovation tourism

Pilots run so someone can say ‘we tried robots’. No one has committed to using them on a real future project even if it works. - Project economics misaligned

One job carries the cost and risk, while many benefits are long-term and organisation-wide. The project team decides the experiment was not worth the pain. - No one assigned to ‘care and feed’

The machine arrives, no one feels responsible, small issues accumulate, and the robot ends up parked ‘for now’. - Bad choice of first project

The first attempt happens on a chaotic, over-constrained site where even basic tasks are barely under control. Robots do not stand a chance.

These stories are not about technology failure alone. They are about misalignment between tool maturity, project readiness and organisational attention.

8. What the next decade probably looks like

Predictions in construction are risky, but a few directions are reasonably clear.

8.1 Where growth is almost guaranteed

- More robots in workflows that already work

Layout, solar trenching and piling, rebar on big decks, structured capture will continue to grow as more contractors gain experience and as products mature. - More trade-centric robots

Specialists in rebar, façade, roofing, interiors and MEP are likely to adopt robots as part of their competitive toolkit, not as science projects. - Closer ties between robots and BIM / planning

Robots will increasingly treat models and schedules as inputs, and their outputs will feed back into digital twins, QA tools and planning systems.

8.2 What could accelerate sharply

- Interiors and MEP robots in repeatable building types

Hotels, student housing, logistics facilities and certain office layouts offer enough repetition and controlled conditions for interior robots to matter. - RaaS and Outcome-based robotics services

Pricing per linear metre, per square metre or per ton, rather than selling machines, can lower adoption barriers if contracts and insurance frameworks adapt. In the near term, Robotics-as-a-Service and outcome-based models are more likely to scale than pure CapEx sales, because they align with how contractors budget and share risk. - Autonomy layers on existing fleets

Software and sensor kits that upgrade existing equipment may expand faster than entirely new machine categories, especially where OEMs and rental houses get onboard.

8.3 What is unlikely in the 2026–2033 window

- Fully autonomous – press start and build a building sites

The complexity, interdependence and human negotiation in live projects make this a long-term aspiration, not a realistic medium-term outcome. - Humanoids as the core jobsite workforce

Humanoids will likely see targeted use in controlled environments and certain factory or logistics roles. On rough, dynamic jobsites, specialised machines will remain the workhorses. - As regulators, safety bodies and insurers (from NIOSH and CPWR to national robotics strategies) start to explicitly reference robotics in guidance and underwriting, the friction around indemnity and liability will drop, especially for robots that clearly remove workers from high-risk tasks.

9. A practical guide for people in the built world

This report is meant to be useful, not just interesting. So we end with three simple questions for GCs, trades and owners.

9.1 Where should you look first?

If you are running or influencing projects, the workflows most worth serious consideration in 2026 are:

- Layout on mid- to large-scale projects with coordinated models

- Solar and energy groundworks on utility-scale projects

- Rebar on large decks, bridges and heavy civil structures

- Regular drone and mobile capture for QA and documentation on complex jobs

These are not speculative any more. There are enough deployments and references to have grounded conversations with vendors and peers.

9.2 How should you start?

A straightforward playbook looks like this:

- Pick one workflow and one project.

Make it a scope you repeat often and can learn from. - Assign one internal owner.

Give them time and support. Do not make this a side project. - Co-design a pilot with clear metrics.

Include production, rework, safety and schedule reliability. Accept that the first deployments are learning exercises. - Plan the robot into the job.

Put tasks on the schedule. Align on digital inputs. Make space, power and access explicit. - Measure and review.

Use both numbers and crew feedback. Decide explicitly whether to scale, pivot or stop.

9.3 What should you ask vendors?

Useful questions often sound like this:

- On how many jobs like ours has this system actually been used?

- Who usually owns it on the contractor side when things go well?

- What do you absolutely need from us in terms of models, survey, access and support?

- How do you support the first few deployments? Who is on site and when?

- How do you use data from our projects to make the product better?

Don’t think of it as buying a machine. You are buying into a workflow and a learning curve.

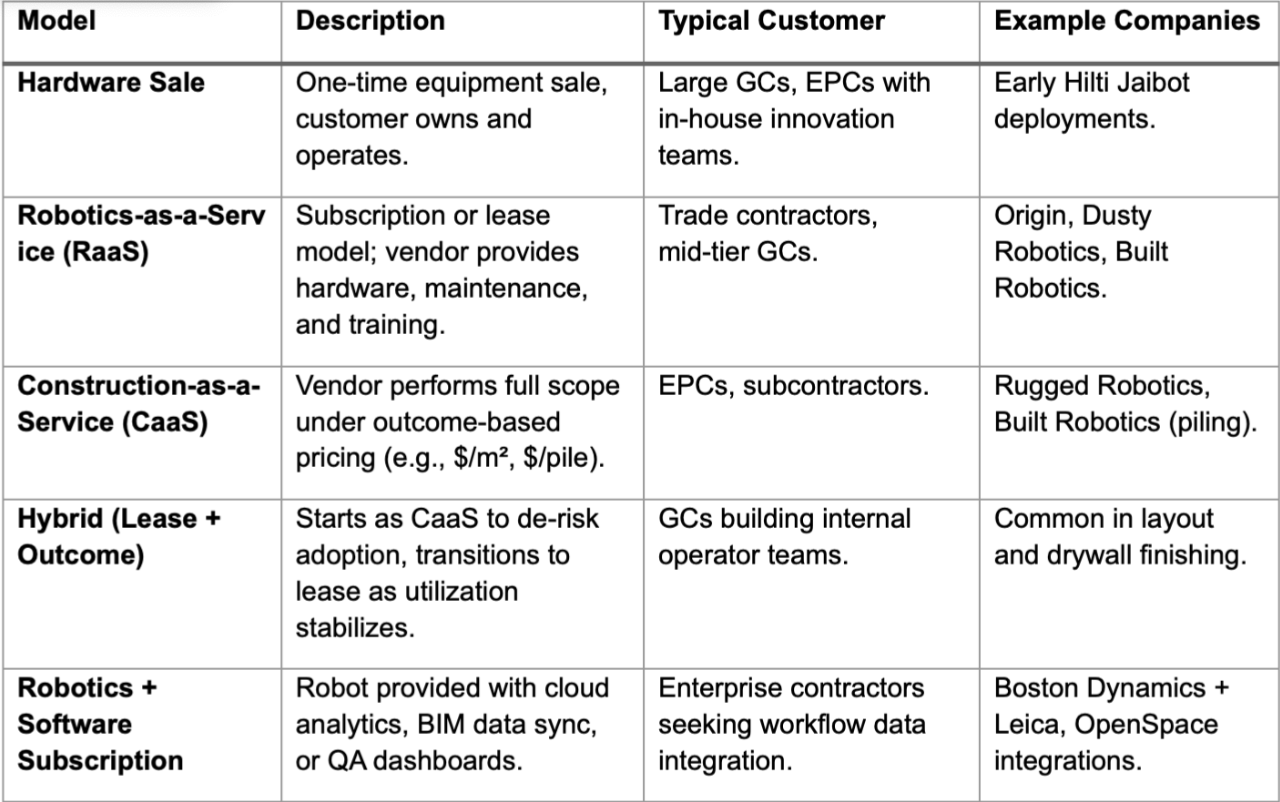

9.4 Business Model Archetypes

10. Closing note

Construction robotics today is not a sci-fi fantasy and not a solved problem. It is a set of specialised tools, built on increasingly capable technology, that can make specific parts of project delivery safer, more predictable and sometimes cheaper.

The opportunity over the next decade is not to chase robotic construction sites as a slogan. It is to:

- Identify the handful of workflows where robots already make sense

- Deploy them with care on the right projects

- Learn fast and share what works and what does not

- Shape the roadmap, so that the next generation of robots reflects the realities of the field, not just the imagination of the lab

If this report helps one superintendent ask sharper questions, one trade contractor choose a good first robot instead of a flashy one, or one founder design a machine that crews actually like working with, it will have done its job.

Contributors

Zacua Ventures Team

- Vivin Hegde

- Varad Mohod

- Margarita de la Peña Virgós

Subham Kedia from Hilti Ventures

Kurt Ramirez, Avi Pradhan from 94 Ventures

References

Market size, macro, and funding

- Oxford Economics & Marsh McLennan. Future of Construction: A Global Forecast for Construction to 2037. Oxford Economics / Marsh, 2023. (Global construction spend and long-term growth outlook.)

- BIS Research. Global Construction Robots Market – Analysis and Forecast, 2023–2033. BIS Research, 2023. (Market sizing and growth rates for construction robotics.)

- Market Research Future. Construction Robotics Market Research Report – Forecast to 2030. Market Research Future, 2023. (Alternate estimate and segmentation of construction robotics market.)

- PitchBook Data, Inc. Construction Technology and Robotics – Custom Dataset for Zacua Ventures, 2017–2025. Proprietary dataset accessed 2025. (Underlying deal counts and funding totals used in the “Venture Funding YOY in Construction Robotics” section.)

- Arcadis. Global Construction Disputes Report 2024. Arcadis, 2024. (Typical dispute values and claims context informing the digital capture / claims-avoidance economics.)

- International Energy Agency (IEA). Renewables 2024 – Analysis and Forecast to 2029. IEA, 2024. (Global solar PV additions and multi-year installation trends underpinning the solar piling opportunity.)

- CPWR – The Center for Construction Research and Training. Robotics and Automation Safety Risks in Construction: A Scoping Review. CPWR / Virginia Tech, 2026. (Overview of safety and risk trends for construction robotics and automation.)

Policy, labour and regional context

- State Council of the People’s Republic of China. Made in China 2025. State Council policy plan, 2015. (Framework for intelligent manufacturing and automation, referenced in regional adoption discussion.)

- Le Monde. “How China is quietly building up its industrial future.” Le Monde, 2024. (Discussion of Made in China 2025 follow-on initiatives and automation push in construction and manufacturing.)

- US Bureau of Labor Statistics (BLS). Labor Force Statistics by Occupation – Construction and Extraction Occupations. BLS, multiple years. (Aging workforce and labour-shortage context.)

- NIOSH (National Institute for Occupational Safety and Health). Robotics and Workplace Safety in Construction – Research Agenda and Workshop Proceedings. NIOSH, 2023. (Safety / robotics guidance referenced in policy tailwinds.)

- CPWR – The Center for Construction Research and Training. Using Robotics and Automation Safely in Construction. CPWR Toolbox Talk series, 2023. (Early guidance on safe deployment of robotics on sites.)

Layout, drywall, interiors and installation robotics

- DPR Construction & Dusty Robotics. “DPR and Dusty Robotics collaborate to set up success for craft.” DPR Construction blog, 2022. (DPR FieldPrinter deployments, layout-cycle compression and multi-trade coordination outcomes.)

- Dusty Robotics. FieldPrinter Product and Case Studies. Dusty Robotics website, accessed 2025. (Throughput, accuracy and floor-area metrics that inform layout productivity and ROI ranges.)

- Canvas. “Canvas and Webcor: Drywall finishing robotics on high-rise projects.” Canvas company case study, 2022. (Evidence for drywall finishing productivity gains and rework reduction.)

- Finish Robotics. Product Overview and Pilot Project Summaries. Finish Robotics website, accessed 2025. (Pilot-to-production trajectory for interior finishing robots.)

- Origin. Origin General-Purpose Interior Robotics Platform. Origin website, accessed 2025. (Description of AI-stacked autonomy, general-purpose interior platform and targeted workflows for drywall and finishes.)

- Raise Robotics. “St. Jude Children’s Research Hospital – Robotics for Facade Brackets and Layout.” Raise Robotics case study, 2024. (10,000+ glass panel positions, layout / drilling / facade installation from one platform.)

Groundworks, civil and solar autonomy

- Built Robotics. “Mortenson: Automating Solar Farm Construction with Built Robotics.” Built Robotics case study, 2023. (Piles-per-day, rework and productivity improvements for solar piling autonomy.)

- Gravis Robotics. Autonomous Excavation and Earthmoving Platform. Gravis Robotics website, accessed 2025. (Description of supervised autonomy modes and Manchester Airport autonomous excavator trial.)

- Teleo. Teleo Supervised Autonomy for Construction Equipment. Teleo website, accessed 2025. (Retrofit autonomy model and supervised-autonomy framing for earthmoving fleets.)

Structural / rebar and heavy concrete

- Advanced Construction Robotics. “Robots on the Koppel Bridge Project.” In Using Robotics and Automation Safely in Construction, CPWR, 2022. (TyBOT tying rates, labour savings and schedule impact on large rebar mats.)

- Brayman Construction & ACR. TyBOT Deployment Summaries on Bridge and Industrial Projects. Brayman Construction published case notes, accessed 2025. (Reinforcing-crew size, duration and ROI ranges.)

- Spacer Robotics. GRID Autonomous Rebar-Tying Robot. Spacer Robotics website, accessed 2025. (Sensor fusion, SLAM / lidar adoption and focus on long-duration tying in congested layouts.)

- Hyperion Robotics / COBOD. 3D-Printed Concrete for Infrastructure and Foundations – Product Literature and Case Studies. Company websites, accessed 2025. (Concrete printing use cases referenced in structural and concrete section.)

MEP, electrical and overhead work

- Hilti. “Hilti Jaibot – Semi-Autonomous Drilling for MEP Layouts.” Hilti Jaibot product and case study page, accessed 2025. (Description of BIM-driven overhead drilling, dust control and labour / ergonomics goals.)

- Hilti & NREL. “Hilti Jaibot at NREL’s Research Support Facility.” Hilti / National Renewable Energy Laboratory project highlight, 2022. (Real-world Jaibot deployment on a complex facility project.)

- Hardhat Robotics. Automated Electrical Installation for Data-Heavy Environments. Hardhat Robotics website, accessed 2025. (Positioning around electrical automation in data centres and similar projects.)

- CSC Robotics and KOBOTS. MEP-Focused Robotics Platforms. Company websites, accessed 2025. (Examples of overhead drilling and cutting automation in MEP workflows.)

Reality capture, inspection and data platforms

- Boston Dynamics & HoloBuilder. “SpotWalk gathers construction data with HoloBuilder and Boston Dynamics.” The Robot Report, 2020. (Hensel Phelps reality-capture deployments using Spot, point clouds and QA progress tracking.)

- Trimble. Spot + Trimble X7: Autonomous 3D Laser Scanning on Construction Sites. Trimble case materials, accessed 2025. (Integration of Spot, Trimble scanners and BIM for automated capture workflows.)

- N Robotics. Mobile Robotics Platform for Construction Sites. N Robotics website, accessed 2025. (Configurable sensor payloads and multi-use capture roles across progress, inspection and environment monitoring.)

- Track3D. Reality Intelligence Platform for Progress Tracking and Deviation Detection. Track3D website, accessed 2025. (Schedule- and BIM-relevant signals built on top of routine capture.)

- OpenSpace. Automated 360° Capture for Construction. OpenSpace website, accessed 2025. (Maturity of scanning / progress-tracking SaaS that informs the “platform absorption” risk.)

Robotics, safety and embodied AI

- International Federation of Robotics (IFR). World Robotics 2024 – Service Robots. IFR, 2024. (Broader robotics context and waves of mobile / data-driven robots.)

- Boston Dynamics. Spot Product Documentation and Case Studies. Boston Dynamics website, accessed 2025. (Jobsite deployment patterns for quadruped robots.)

- NVIDIA. Isaac Sim – Robotics Simulation for AI-Powered Robots. NVIDIA developer documentation, accessed 2025. (Simulation and sim-to-real tooling referenced in the technology stack section.)

- Okpala, I. et al. “Insidious risks of wearable robots to worker safety and health.” Journal of Safety Research, 2024. (Risk / safety considerations for construction wearables and robotics.)

Disputes, claims and documentation

- Marsh McLennan. Global Construction Risk Report 2024. Marsh, 2024. (Context on frequency and cost of disputes and claims, supporting the claims-avoidance value ranges in the digital capture economics.)

- Arcadis. Global Construction Disputes Report 2023. Arcadis, 2023. (Historical dispute costs and patterns used to ground conservative claim-avoidance assumptions.)